Page 51 - AOB 2018 (ENG)

P. 51

Audit

Oversight

Board

ANNUAL

REPORT

2018

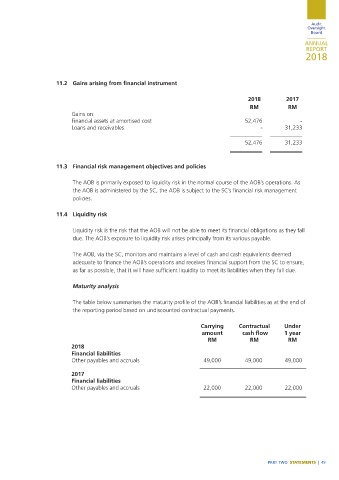

11.2 Gains arising from financial instrument

2018 2017

RM RM

Gains on:

Financial assets at amortised cost 52,476 -

Loans and receivables - 31,233

52,476 31,233

11.3 Financial risk management objectives and policies

The AOB is primarily exposed to liquidity risk in the normal course of the AOB’s operations. As

the AOB is administered by the SC, the AOB is subject to the SC’s financial risk management

policies.

11.4 Liquidity risk

Liquidity risk is the risk that the AOB will not be able to meet its financial obligations as they fall

due. The AOB’s exposure to liquidity risk arises principally from its various payable.

The AOB, via the SC, monitors and maintains a level of cash and cash equivalents deemed

adequate to finance the AOB’s operations and receives financial support from the SC to ensure,

as far as possible, that it will have sufficient liquidity to meet its liabilities when they fall due.

Maturity analysis

The table below summarises the maturity profile of the AOB’s financial liabilities as at the end of

the reporting period based on undiscounted contractual payments.

Carrying Contractual Under

amount cash flow 1 year

RM RM RM

2018

Financial liabilities

Other payables and accruals 49,000 49,000 49,000

2017

Financial liabilities

Other payables and accruals 22,000 22,000 22,000

PART TWO STATEMENTS | 49

T_2018 AOB AR PART 2.indd 49 10/04/2019 5:11 PM