Page 38 - Inspection Report 2018

P. 38

Audit firms should assess and consider whether the finding is actually a symptom of a wider issue that needs

to be addressed promptly and effectively.

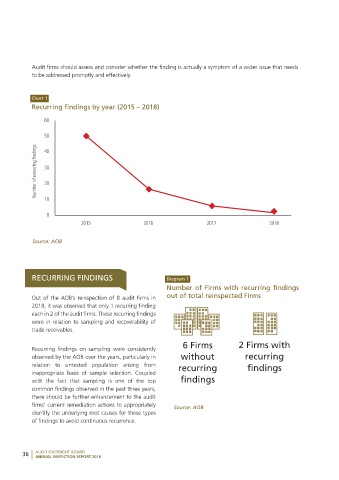

Chart 1

recurring findings by year (2015 – 2018)

60

50

Number of recurring findings 30

40

20

10

0

2015 2016 2017 2018

Source: AOB

rECurrING FINdINGS diagram 1

Number of Firms with recurring findings

Out of the AOB’s reinspection of 8 audit firms in out of total reinspected Firms

2018, it was observed that only 1 recurring finding

each in 2 of the audit firms. These recurring findings

were in relation to sampling and recoverability of

trade receivables.

6 Firms 2 Firms with

Recurring findings on sampling were consistently

observed by the AOB over the years, particularly in without recurring

relation to untested population arising from recurring findings

inappropriate basis of sample selection. Coupled

with the fact that sampling is one of the top findings

common findings observed in the past three years,

there should be further enhancement to the audit

firms’ current remediation actions to appropriately Source: AOB

identify the underlying root causes for these types

of findings to avoid continuous recurrence.

AUDIT OVERSIGHT BOARD

36 ANNUAL INSPECTION REPORT 2018

83806_Inside_NEW.indd 36 5/28/19 3:02 PM