Page 82 - SC Annual Report 2018 (ENG)

P. 82

Securities

Commission

Malaysia

ANNUAL

REPORT

2018

Chart 1

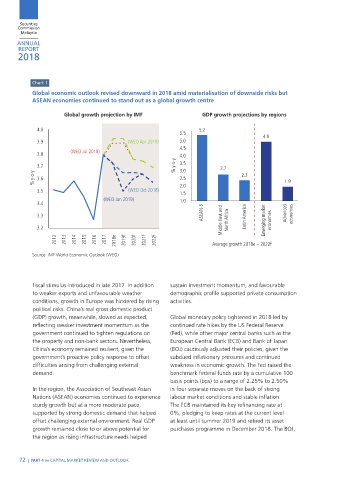

Global economic outlook revised downward in 2018 amid materialisation of downside risks but

ASEAN economies continued to stand out as a global growth centre

Global growth projection by IMF GDP growth projections by regions

4.0 5.2

5.5 4.8

3.9 (WEO Apr 2018) 5.0

4.5

(WEO Jul 2018)

3.8 4.0

3.7 % y-o-y 3.5 2.7

3.0

% y-o-y 3.6 2.5 2.3 1.9

3.5 (WEO Oct 2018) 2.0

1.5

(WEO Jan 2019) 1.0

3.4

ASEAN-5 Advanced

3.3 Middle East and North Africa Latin America Emerging market economies economies

3.2

2012 2013 2014 2015 2016 2017 2018e 2019f 2020f 2021f 2022f Average growth 2018e – 2022f

Source: IMF World Economic Outlook (WEO)

fiscal stimulus introduced in late 2017. In addition sustain investment momentum, and favourable

to weaker exports and unfavourable weather demographic profile supported private consumption

conditions, growth in Europe was hindered by rising activities.

political risks. China’s real gross domestic product

(GDP) growth, meanwhile, slowed as expected, Global monetary policy tightened in 2018 led by

reflecting weaker investment momentum as the continued rate hikes by the US Federal Reserve

government continued to tighten regulations on (Fed), while other major central banks such as the

the property and non-bank sectors. Nevertheless, European Central Bank (ECB) and Bank of Japan

China’s economy remained resilient, given the (BOJ) cautiously adjusted their policies, given the

government’s proactive policy response to offset subdued inflationary pressures and continued

difficulties arising from challenging external weakness in economic growth. The Fed raised the

demand. benchmark federal funds rate by a cumulative 100

basis points (bps) to a range of 2.25% to 2.50%

In the region, the Association of Southeast Asian in four separate moves on the back of strong

Nations (ASEAN) economies continued to experience labour market conditions and stable inflation.

sturdy growth but at a more moderate pace, The ECB maintained its key refinancing rate at

supported by strong domestic demand that helped 0%, pledging to keep rates at the current level

offset challenging external environment. Real GDP at least until summer 2019 and retired its asset

growth remained close to or above potential for purchases programme in December 2018. The BOJ,

the region as rising infrastructure needs helped

72 | PART 4 »» CAPITAL MARKET REVIEW AND OUTLOOK

NEW_70-89.indd 72 2/21/19 9:29 AM