Page 85 - SC Annual Report 2018 (ENG)

P. 85

Securities

Commission

Malaysia

ANNUAL

REPORT

2018

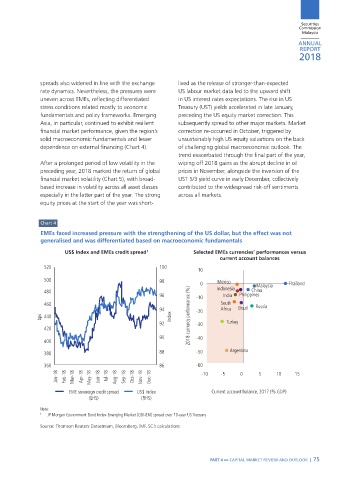

spreads also widened in line with the exchange lived as the release of stronger-than-expected

rate dynamics. Nevertheless, the pressures were US labour market data led to the upward shift

uneven across EMEs, reflecting differentiated in US interest rates expectations. The rise in US

stress conditions related mostly to economic Treasury (UST) yields accelerated in late January,

fundamentals and policy frameworks. Emerging preceding the US equity market correction. This

Asia, in particular, continued to exhibit resilient subsequently spread to other major markets. Market

financial market performance, given the region’s correction re-occurred in October, triggered by

solid macroeconomic fundamentals and lesser unsustainably high US equity valuations on the back

dependence on external financing (Chart 4). of challenging global macroeconomic outlook. The

trend exacerbated through the final part of the year,

After a prolonged period of low volatility in the wiping off 2018 gains as the abrupt decline in oil

preceding year, 2018 marked the return of global prices in November, alongside the inversion of the

financial market volatility (Chart 5), with broad- UST 5/3 yield curve in early December, collectively

based increase in volatility across all asset classes contributed to the widespread risk-off sentiments

especially in the latter part of the year. The strong across all markets.

equity prices at the start of the year was short-

Chart 4

EMEs faced increased pressure with the strengthening of the US dollar, but the effect was not

generalised and was differentiated based on macroeconomic fundamentals

US$ Index and EMEs credit spread 1 Selected EMEs currencies’ performances versus

current account balances

520 100

10

500 98 0 Mexico Malaysia Thailand

480 Indonesia China

96 -10 India Philippines

460 South Russia

94 -20 Africa Brazil

bps 440 Index 2018 currency performance (%)

92 -30 Turkey

420

90 -40

400

380 88 -50 Argentina

360 86 -60

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 -10 -5 0 5 10 15

EME sovereign credit spread US$ Index Current account balance, 2017 (% GDP)

(LHS) (RHS)

Note:

1 JP Morgan Government Bond Index-Emerging Market (GBI-EM) spread over 10-year US Treasury

Source: Thomson Reuters Datastream, Bloomberg, IMF, SC’s calculations

PART 4 »» CAPITAL MARKET REVIEW AND OUTLOOK | 75

NEW_70-89.indd 75 2/21/19 9:29 AM