Page 97 - SC Annual Report 2018 (ENG)

P. 97

Securities

Commission

Malaysia

ANNUAL

REPORT

2018

could affect investor sentiments, heighten market central banks, including the Fed, to communicate

volatility and disrupt global trade networks, thus that the future pace of monetary tightening will

affecting overall economic performance. Over the likely be gradual and data-dependent. The flattening

longer term, persistent trade uncertainties could trend of the global bond yield curves will likely

hit real investment activities that may lead to an persist, catalysed by higher global risk aversion.

even lower economic growth potential because

of limited productive capacity. While some Asian On the other hand, the prospects of global equities

economies, including Malaysia, may benefit from the are expected to remain subdued, given persistently

reconfiguration of the global trade production chain, stretched valuations in selected key markets and

all economies stand to lose due to overall weaker diminishing earnings growth outlook. Meanwhile,

global trade and investment activities. credit spreads between EMEs and AEs are projected

to remain relatively contained, amid the possible

The global capital markets will also be characterised turnaround in global portfolio flows favouring EMEs’

by the ongoing shift in global financial liquidity, assets as a result of a potentially less aggressive

mainly driven by developed markets’ monetary Fed. However, investors’ appetite towards EMEs’

policy normalisation. However, heightened downside assets are likely to remain selective and in favour of

risks to global growth have induced most major economies with strong fundamentals.

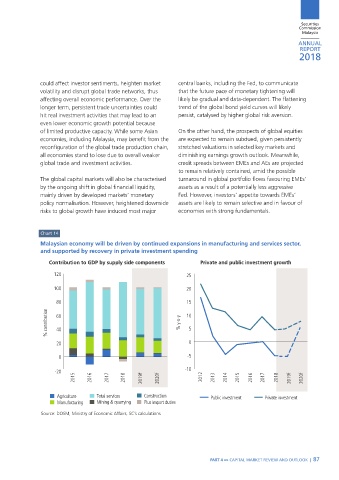

Chart 14

Malaysian economy will be driven by continued expansions in manufacturing and services sector,

and supported by recovery in private investment spending

Contribution to GDP by supply side components Private and public investment growth

120 25

100 20

80 15

% contribution 60 % y-o-y 10

5

40

20 0

0 -5

-20 -10

2015 2016 2017 2018 2019f 2020f 2012 2013 2014 2015 2016 2017 2018 2019f 2020f

Agriculture Total services Construction Public investment Private investment

Manufacturing Mining & quarrying Plus import duties

Source: DOSM, Ministry of Economic Affairs, SC’s calculations

PART 4 »» CAPITAL MARKET REVIEW AND OUTLOOK | 87

NEW_70-89.indd 87 2/21/19 9:29 AM