Page 98 - SC Annual Report 2018 (ENG)

P. 98

Securities

Commission

Malaysia

ANNUAL

REPORT

2018

Domestically, against the backdrop of a more Meanwhile, trading activities in the secondary

challenging and uncertain global environment, market will continue to be driven by external

the Malaysian economy is anticipated to remain developments, mainly movements in portfolio flows

on a steady growth path, backed by firm domestic arising from the shift in global liquidity and the

private sector activities (Chart 14). Growth will be general increase in global financial market volatility.

underpinned by sustained manufacturing activities

and further supported by resilient services sector Notably, the developments observed in the

expansion, especially in wholesale and retail trade aftermath of the GFC indicate that the underlying

sub-sectors. On the demand side, steady wage and trend movement in non-resident portfolio flows

employment growth will continue to drive private was, to a large extent, determined by major central

consumption expansion while new and ongoing banks’ monetary policy directions, especially the Fed

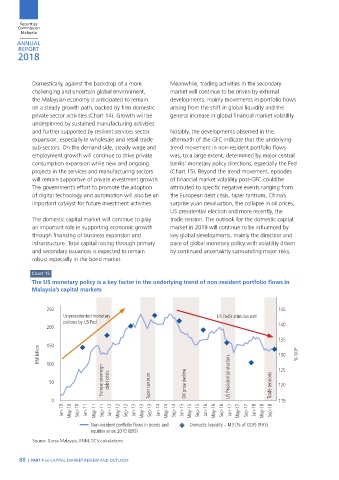

projects in the services and manufacturing sectors (Chart 15). Beyond the trend movement, episodes

will remain supportive of private investment growth. of financial market volatility post-GFC could be

The government’s effort to promote the adoption attributed to specific negative events ranging from

of digital technology and automation will also be an the European debt crisis, taper tantrum, China’s

important catalyst for future investment activities. surprise yuan devaluation, the collapse in oil prices,

US presidential election and more recently, the

The domestic capital market will continue to play trade tension. The outlook for the domestic capital

an important role in supporting economic growth market in 2019 will continue to be influenced by

through financing of business expansion and key global developments, mainly the direction and

infrastructure. Total capital raising through primary pace of global monetary policy with volatility driven

and secondary issuances is expected to remain by continued uncertainty surrounding major risks,

robust especially in the bond market.

Chart 15

The US monetary policy is a key factor in the underlying trend of non-resident portfolio flows in

Malaysia’s capital markets

250 145

Unprecedented monetary US Fed’s stimulus exit

policies by US Fed

200 140

135

150

RM billion 100 130 % GDP

Europe sovereign debt crisis US Presidential election 125

50 Taper tantrum Oil price decline Trade tensions 120

0 115

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18

Non-resident portfolio flows in bonds and Domestic liquidity – M3 (% of GDP) (RHS)

equities since 2010 (LHS)

Source: Bursa Malaysia, BNM, SC’s calculations

88 | PART 4 »» CAPITAL MARKET REVIEW AND OUTLOOK

NEW_70-89.indd 88 2/21/19 9:29 AM